Rebuilding After Wildfires in Los Angeles County

Wildfires have wreaked havoc on countless homes and businesses across Los Angeles County, leaving property owners struggling to...

Read more

Discovering that an uninsured driver caused your accident in Fallbrook is devastating enough. Learning that your own insurance company has denied your uninsured motorist claim denied feels like a betrayal. You paid premiums faithfully, trusted your insurer to protect you, and now they refuse to honor their commitment when you need them most. This situation is more common than you might think, and you have legal options to fight back.

In my experience representing injured drivers throughout North San Diego County, I see these claim denials far too often. Insurance companies use various tactics to avoid paying legitimate claims, from questioning the severity of injuries to disputing that the other driver was truly uninsured. Understanding why claims get denied and what steps to take next can make the difference between accepting an unfair denial and recovering the compensation you deserve.

Insurance companies are businesses focused on profit margins, not customer welfare. They employ teams of adjusters, investigators, and attorneys whose job is to minimize payouts. Here are the most common reasons insurers deny these claims in California:

Questioning Coverage Existence

Your insurer may claim you never purchased coverage or that your policy lapsed. They might argue that you declined the coverage in writing, even though California law requires insurers to offer it. This tactic particularly affects drivers who speak Spanish as their primary language and may not have fully understood policy documents.

Disputing the Other Driver’s Insurance Status

Insurance companies often investigate whether the at-fault driver actually lacked coverage. They may discover the other driver had insurance that expired days before your accident, then argue the driver was technically insured at the time of the crash. These technicalities allow insurers to shift responsibility to another company.

Claiming Insufficient Evidence of Fault

Even with coverage, you must prove the other driver caused your accident. If the San Diego County Sheriff’s Department report is inconclusive, or if there were no witnesses to an accident on a rural stretch of Old Highway 395, your insurer may deny the claim based on disputed liability.

Minimizing Injury Severity

Insurance companies frequently argue that your injuries aren’t as severe as claimed or weren’t caused by the accident. They scrutinize medical records, demand independent medical examinations, and question treatment recommendations to reduce claim values.

Consider a situation where a driver gets rear-ended by an uninsured motorist during heavy commute traffic on Highway 76 near Pala Casino Road. The victim develops symptoms days later, but the insurance company denies the claim, arguing that delayed symptom onset proves the injuries weren’t caused by the accident. In reality, soft tissue injuries and concussions often have delayed presentations, and California law recognizes this medical fact. These accidents typically result in whiplash, herniated discs, and traumatic brain injuries. Under California Vehicle Code Section 17151, uninsured drivers are still liable for damages, and your own coverage should compensate you.

Another frequent scenario occurs at busy intersections like Mission Road and Ammunition Road, where an uninsured driver runs a red light and causes a T-bone collision. The victim suffers fractured ribs, internal bleeding, and shoulder injuries common in side-impact crashes. They file a claim, but the insurance company hires private investigators to prove the other driver actually had coverage through a different carrier. Even when the other driver admits to being uninsured, insurers spend thousands on investigations to avoid paying legitimate claims for serious injuries.

Hit-and-run accidents create additional challenges. If someone hits you on a poorly lit section of South Mission Road near the Fallbrook Community Center and flees the scene, your insurer may deny the claim arguing you cannot prove the other driver was uninsured. California Vehicle Code Section 20001 makes hit-and-run a felony, but proving the phantom driver lacked insurance becomes nearly impossible without identifying them.

California Insurance Code Section 11580.2 requires insurance companies to offer coverage to all drivers. If you didn’t specifically decline this coverage in writing, you have it automatically. This law protects consumers, but insurance companies often ignore these protections hoping customers won’t fight back.

California also follows comparative negligence rules under Civil Code Section 1431.2. Even if you were partially at fault for your accident, you can still recover damages through your coverage. For example, if you were 20% at fault for an intersection accident and the uninsured driver was 80% at fault, you can still recover 80% of your damages from your own insurer.

The statute of limitations for these claims is typically two years from the date of the accident under Code of Civil Procedure Section 335.1. However, your insurance policy may contain shorter deadlines for reporting claims or filing lawsuits, making prompt action essential.

Your insurance policy is a contract, and insurance companies must handle claims in good faith under California’s implied covenant of good faith and fair dealing. When insurers deny valid claims without reasonable basis, they may be liable for bad faith damages beyond your original claim value.

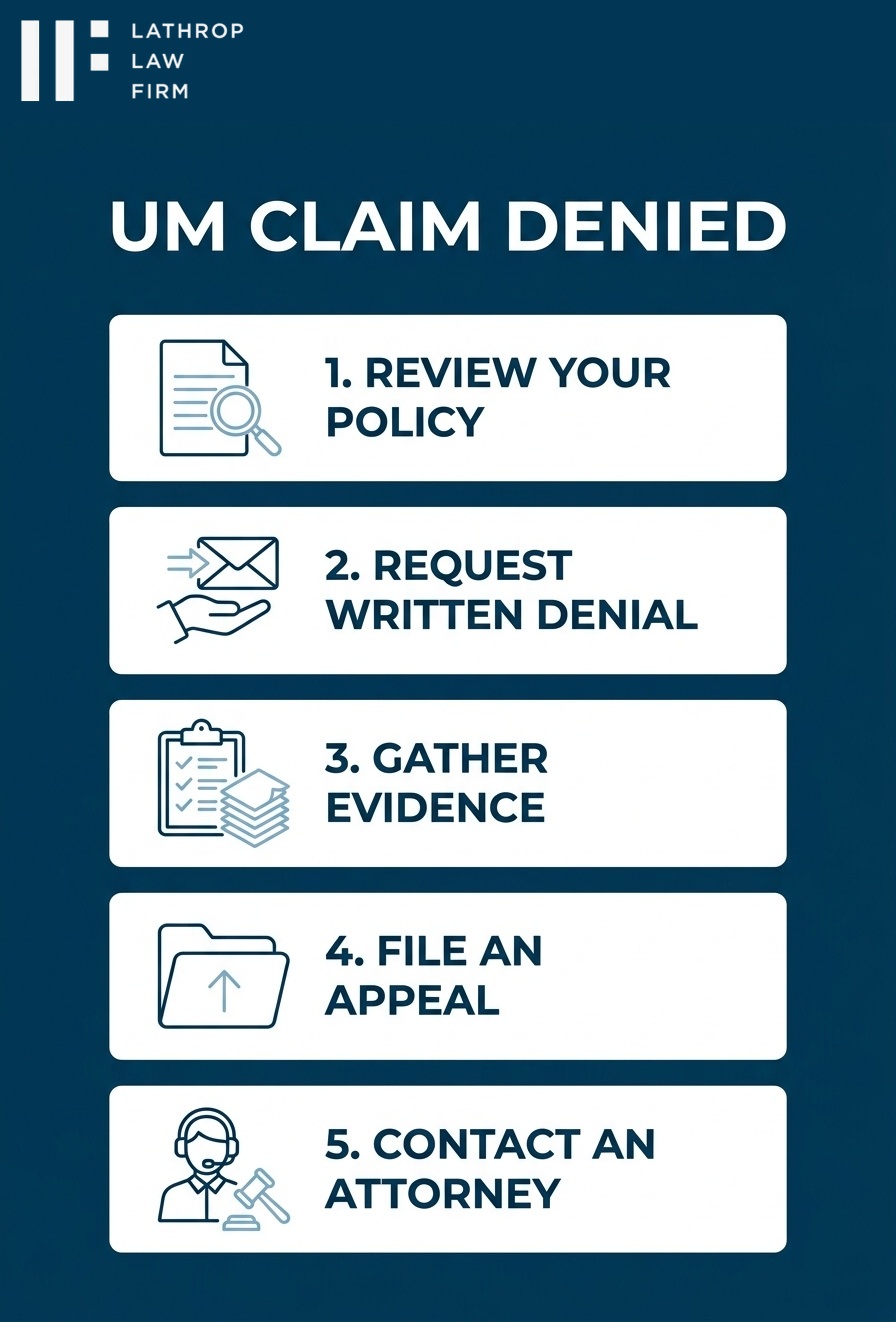

Don’t accept a claim denial as final. Insurance companies count on customers giving up after receiving denial letters. Here’s what you should do immediately:

Request the Complete Claim File

California law gives you the right to review your entire claim file. Request all documents, photographs, recorded statements, medical records, and correspondence. This file often reveals the real reasons for denial and may contain evidence supporting your claim.

Get the Denial in Writing

If the insurance company denied your claim verbally, demand written confirmation stating specific reasons for the denial. Vague or generic denial letters may indicate the insurer lacks valid grounds for denial.

Document Everything

Keep detailed records of all communications with your insurance company. Note dates, times, names of representatives, and summaries of conversations. If representatives make promises or admissions, follow up with written confirmation.

Continue Medical Treatment

Don’t stop treating your injuries because your claim was denied. Gaps in treatment allow insurance companies to argue you weren’t really hurt. Follow your doctor’s recommendations and keep all medical appointments.

Most insurance policies include internal appeal processes before you can file a lawsuit. Use this process strategically to strengthen your position:

Gather Additional Evidence

Collect any evidence that wasn’t available when you first filed your claim. This might include additional witness statements, surveillance footage from businesses near the accident scene, or medical records confirming your diagnosis.

Get Expert Medical Opinions

If the insurance company disputes your injuries, consider getting an independent medical evaluation from a qualified physician. Choose doctors who regularly testify in personal injury cases and understand the relationship between accident forces and resulting injuries.

Document Financial Losses

Calculate all economic damages from the accident, including medical bills, lost wages, property damage, and ongoing treatment costs. Include documentation like pay stubs, tax returns, and employment records to prove your income losses.

Address Each Denial Reason

Structure your appeal to address every reason cited in the denial letter. If the insurer questions coverage, provide policy documents proving coverage existed. If they dispute fault, provide additional evidence of the other driver’s negligence.

If your insurance company maintains its denial after a thorough internal appeal, filing a lawsuit may be your only option to recover compensation. Several factors indicate it’s time to consider litigation:

The denial appears to be in bad faith, with no reasonable basis for rejecting your claim. Insurance companies must investigate claims fairly and cannot deny valid claims simply to save money.

Your injuries are severe enough to justify the cost and time involved in litigation. Catastrophic injury cases often require legal action because insurance companies rarely offer fair settlements for life-changing injuries.

The insurance company is treating you unfairly during the claims process, such as demanding unreasonable documentation, delaying investigations, or making lowball settlement offers after initially denying the claim.

You’re approaching the statute of limitations deadline and need to preserve your legal rights. Don’t wait until the last minute, as preparing a strong case takes time.

California law requires insurance companies to handle claims promptly, thoroughly, and fairly. When insurers violate these duties, they may be liable for bad faith damages. Common bad faith practices include:

Denying claims without conducting reasonable investigations. If your insurer denies your claim without properly investigating the accident circumstances or your injuries, they may be acting in bad faith.

Misrepresenting policy language or coverage terms. Some insurers tell customers they lack coverage when they actually have it, or they misinterpret policy language to avoid paying claims.

Failing to communicate effectively with policyholders. Insurance companies must keep you informed about claim status and explain decisions clearly. Refusing to return phone calls or provide claim updates may constitute bad faith.

Setting unreasonable deadlines or making excessive demands for documentation. While insurers can request reasonable proof of loss, they cannot make impossible demands designed to frustrate the claims process.

Insurance companies have entire legal departments dedicated to denying and defending claims. Facing these resources alone puts you at a significant disadvantage. As a Fallbrook car accident attorney with years of experience fighting insurance companies, I understand their tactics and know how to build compelling cases for denied claims.

An experienced attorney can review your policy language, investigate the denial reasons, and determine whether your insurance company acted in bad faith. I can also coordinate with medical experts to document your injuries and calculate the full extent of your damages.

In these cases, the relationship between you and your own insurance company changes from customer-provider to adversaries. Having legal representation protects your interests and ensures you’re not taken advantage of during this vulnerable time.

Most importantly, I work on a contingency fee basis for dealing with insurance companies, meaning you pay no attorney fees unless I recover compensation for your denied claim. This arrangement allows you to fight back against unfair denials without upfront legal costs.

If your claim has been denied in Fallbrook, don’t give up. As a bilingual attorney practicing in North San Diego County, I can help you understand your rights and fight for the coverage you paid for. Contact my office today for a free consultation to discuss your denied claim and explore your legal options. Hablo español y estoy aquí para ayudarle en este momento difícil.